Think Small?

Investing in small caps

Small-cap investing is a marathon, not a sprint. It requires patience, discipline, and a long-term perspective. – Chuck Royce

Let’s start with a quick poll:

In 1970, Eugene Fama published a paper titled "Efficient Capital Markets: A Review of Theory and Empirical Work" in The Journal of Finance which introduced the concept of the efficient market hypothesis (EMH). The basic tenet of EMH is that the financial markets are perfectly efficient and that the prices in the market fully reflect all available information about the company. If the efficient market hypothesis holds, it is impossible to consistently beat the market by using any information or analysis, because the stock price already captures all such information.

But just 12 years later, Rolf Banz1 published a report which showed that small stocks had consistently higher average risk-adjusted returns that the efficient market hypothesis could not explain.2 If some specific assets can generate higher returns than the market without taking on additional risk, then the market is clearly mispricing those stocks. Fama eventually explained this outperformance using the small firm effect in the Fama-French three-factor model.

The small firm effect is simple in theory - smaller companies have a greater amount of growth opportunities than larger companies, at the same time having a smaller base. Apple adding a couple of billion to its bottom line by launching a new product line would barely move its stock price but a small-cap stock announcing a new patent or drug approval is enough to double its stock price overnight.

In addition, small-cap companies are barely covered by analysts, leading to large inefficiencies. Popular companies like Apple, Google, Tesla, etc. are covered by 100s of analysts every quarter whereas there would be small-cap companies that are not even covered by a single analyst.

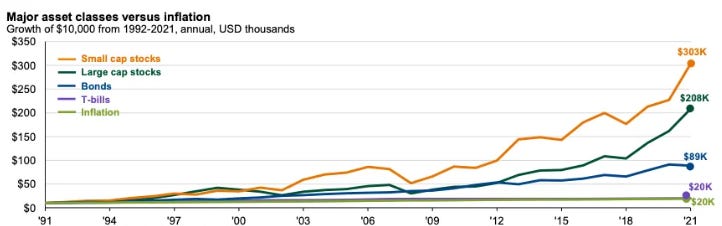

The flip side is that since these companies are small, there is a higher chance of them going bust due to mismanagement or harsh economic conditions. All of this means that you are taking some extra risk by investing in small-cap stocks and should be rewarded with higher-than-market returns. Data proves the same – Over the past 90 years, small stocks have outperformed their large counterparts by 1.88% annually. While it does not sound like much, over time the returns add up substantially. Since 1990, small-cap stocks have outperformed large-cap stocks by 45%.

But, it’s not all sunshine and rainbows in the world of small-cap investing. Even though over the long term small caps have outperformed S&P 500, there would be long periods of underperformance. The last ~10 years have not been great for small caps as they have underperformed the S&P 500.

Adding to this, small-cap stocks are impacted more than their large-cap counterparts during market drawdowns. But the silver lining here is that during the rebound, they come back stronger.

While it might look like an attractive time to get into small caps, it’s important to consider

If small-cap investing still works or if the advantage has been arbitraged away by high-frequency traders and easier access to data?

What’s the ideal proportion of small-cap companies in your portfolio?

Downsides/risks with small caps?

The best available small-cap ETFs & if we can improve upon traditional small-cap investing by adding one or two factors like profitability and PE ratios?

Let’s dig in: