Multifactor diversification

The theory and practice

Hey, thanks for reading Market Sentiment! We have a small request – if you enjoy reading our articles, please like the article and share it with someone you think might enjoy this. This helps with our ranking and lets more people see our work.

In the 1952 Journal of Finance, Harry Markowitz introduced some ideas in his paper “Portfolio Theory” which tried to answer this question: Given a level of risk, how can expected return be maximized? The ideas outlined in that paper were adopted slowly at first, but went on to form the basis of Modern Portfolio Theory which institutional investors rely on heavily to select investments.

The idea of diversification was a consequence of this paper. 80% of all stocks have had negative returns and selecting stocks for their future performance is improbable. But by selecting two uncorrelated stocks, the chances of a loss drop dramatically. The more uncorrelated stocks you have in your portfolio, the lesser the chances of a drawdown. This is essentially the idea behind indexing.

{kind=link}

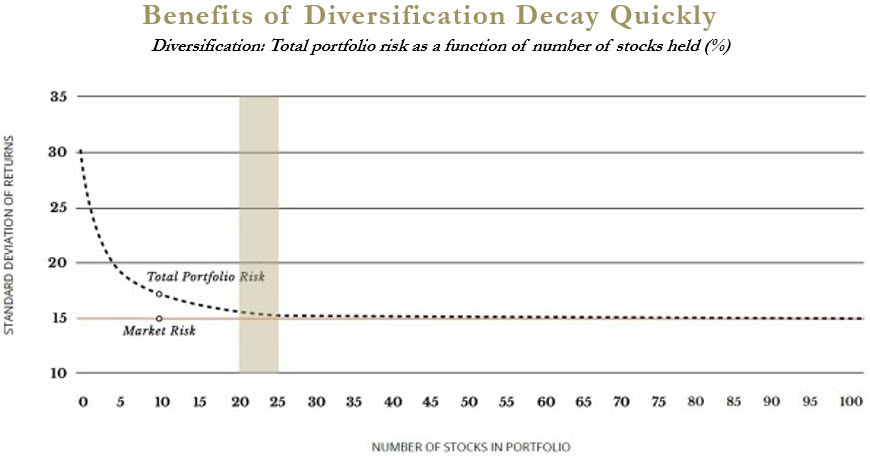

But this protection against risk comes at a cost. In his book A random walk on Wall Street, Burton Malkiel showed that after the 5th stock, the benefits of diversification begin to wane and after the 20th stock, adding even 100 more stocks doesn’t reduce volatility – but it eats away at returns. Naive diversification has limited benefits. In today’s report, let’s dive into:

Why is indexing not “true” diversification?

Are multi-factor funds a better way to capture returns while minimizing risks?

What are the implementation challenges for individual investors?

A diversification strategy that works across economic cycles