Investing in moats

Can economic moats lead to excess shareholder value?

Welcome to Market Sentiment. We curate the best ideas from thousands of research sources and distill them into weekly actionable insights. Based on last week’s ideastorm poll, 43% of you voted for a deep dive on Moats.

If you are new here, join 35,000+ others who receive curated financial research.

Actionable Insights

The company's size is not representative of its moat or long-term competitive advantage — of the 500 companies published in the first ever Fortune 500 list, only 52 made it to 2022.

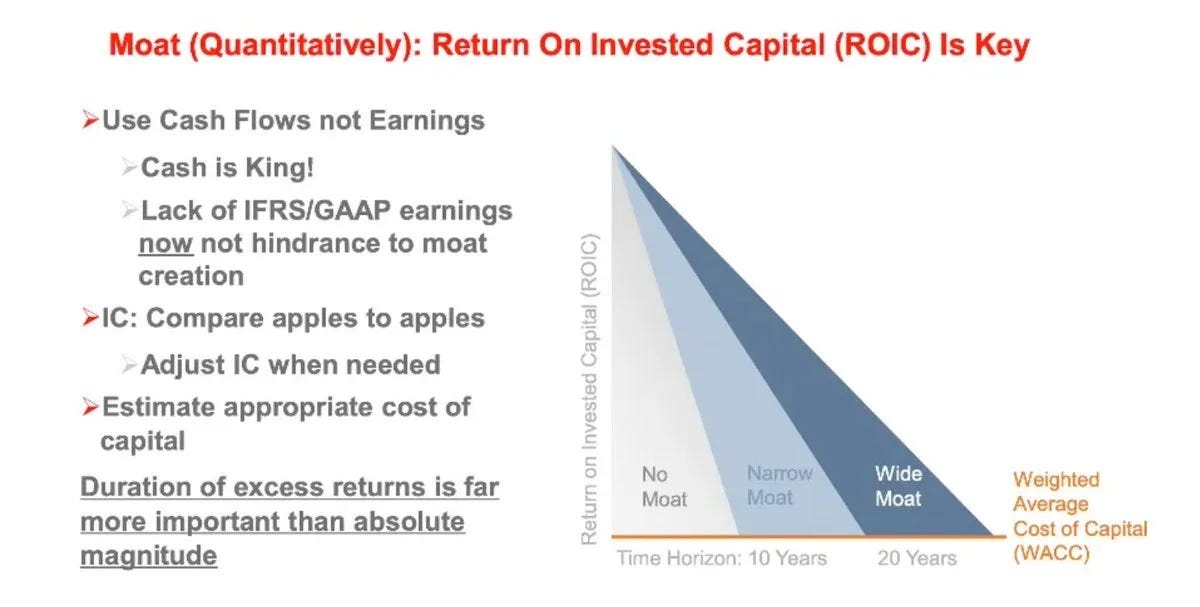

ROIC (Return on Invested Capital) is a crucial metric for evaluating moat. If the company has generated higher returns on their investment than the cost of capital, the returns are bound to come back to shareholders.

Wide moat stock1 portfolios were able to beat both the S&P 500 and Russell 3000 by a significant margin while having lower volatility (2002-2014)2

VanEck Morningstar Wide Moat ETF has outperformed the S&P 500 on a risk-adjusted basis over the last ten years (325% vs 278% return)

If you gave me $100 billion and said take away the soft drink leadership of Coca-Cola in the world, I'd give it back to you and say it can't be done. - Warren Buffett

Buffett was one of the first to popularize the concept of economic moats with his 2007 letter to Berkshire shareholders.

A truly great business must have an enduring “moat” that protects excellent returns on invested capital. The dynamics of capitalism guarantee that competitors will repeatedly assault any business “castle” that is earning high returns.

Therefore a formidable barrier such as a company’s being the low-cost producer (GEICO, Costco) or possessing a powerful world-wide brand (Coca-Cola, Gillette, American Express) is essential for sustained success. Business history is filled with “Roman Candles,” companies whose moats proved illusory and were soon crossed.

Buffett walks the talk by mainly investing in companies having incredible moats. One of our personal favorites from his portfolio is FlightSafety. The company was started in 1951 and provides flight training for pilots. Berkshire acquired FlightSafety in 1996 & Buffett argued that it had one of the best durable competitive advantages: Being a pilot is a highly skilled job with no room for error. Anyone who wishes to be a pilot would like to be trained by the best, and FlightSafety is arguably the best flight-training provider. In Buffett’s own words

Going to any other flight-training provider than the best is like taking the low bid on a surgical procedure.

On the other hand, talking about companies whose moats proved illusory, the first ever Fortune 500 list was created by Edgar P. Smith and published in 1955. A look at the list over the years shows incredible churn; of the 500 companies in 1955, only 52 made it to 2022.

Think about that for a minute – These are not fly-by-night companies hoping they make it to the following year. These were some of the world’s largest companies, and only 1 in 10 stayed on the list after six decades. Nearly 2,000 companies have appeared on the list since its inception, and most of them are now unrecognizable, forgotten companies today (e.g., Chrysler, Teledyne, Bethlehem Steel, etc.).

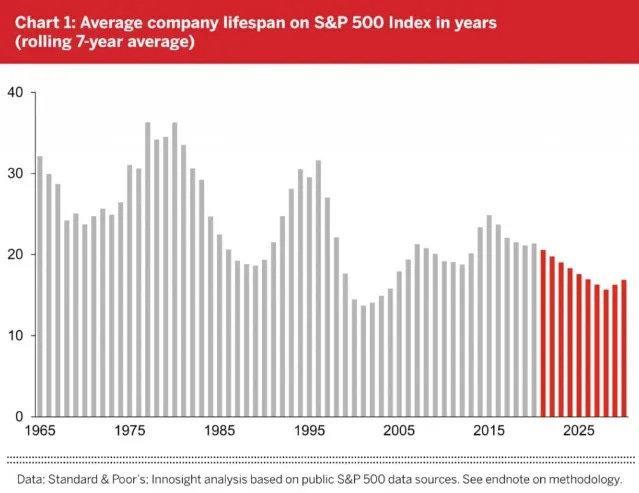

The average lifespan of a company on the S&P 500 list is continuously dropping and is now only 15 years compared to the 30 years in the ’80s. It’s only reasonable to assume that the list released 60 years from now would be wildly different from what it currently is

Given the ever-growing churn in the top companies, investing in companies with durable competitive advantages becomes crucial.

Identifying companies with a moat

Michael Porter was the first to highlight the importance of a company establishing and maintaining a competitive advantage with his Five Forces Framework. The bargaining power with suppliers & buyers, threats from new entrants/substitutes, and industry rivalry all played a part in evaluating the attractiveness of a particular industry. Simply put, companies with a solid moat can keep their competitors at bay for an extended period while generating outsized returns for their shareholders.

Morningstar is one of the key players providing data related to moats with their economic moat rating. They look for companies that have generated a higher return on invested capital (than the cost of capital) for a long time. The logic is simple – If the company has generated higher returns on their investment than the cost of capital, the returns are bound to come back to shareholders.

But, since ROIC (Return on Invested Capital) is just one historical metric, using that alone won’t get us the full picture. To combat this, Morningstar uses ROIC in association with

Network Effect: It’s the classic case where growth begets more growth. Think eBay. The more sellers there are on eBay, the more likely buyers will find what they’re looking for at a decent price. The more buyers there are, the easier it is to sell things.

Intangible Assets: Intangible assets like patents, brands, licensing, etc. are key to preventing competition from taking your market share. We have already shown that the world’s most reputable brands were able to beat the market. Companies like American Express, Apple, and BMW have high pricing power due to their strong brands

Cost Advantage: Firms with massive inventories like Costco & Amazon will be able to undercut competitors on price while earning similar margins.

Switching Costs: If it’s too expensive or troublesome to stop using a company’s product (Adobe, Salesforce, Oracle, etc.), the company will often have a high pricing power that leads to higher margins.

Efficient Scale: If the market is served only by a few companies, it creates a pseudo-oligopolistic market. It would be too expensive/cumbersome for a new player to enter and disrupt the market. Classic examples would be online search (Google is virtually a monopoly) & shipping companies like UPS/FedEx.

It’s not necessary for a company to have all of the above considered a wide moat. Morningstar defines the moat as a spectrum.

A company whose competitive advantages we expect to last more than 20 years has a wide moat; one that can fend off their rivals for 10 years has a narrow moat; while a firm with either no advantage or one that we think will quickly dissipate has no moat.

Do companies with a wide moat outperform? (and the performance of VanEck Morningstar Wide Moat ETF)

Kanuri et al. (Applied Economics) evaluated the performance of wide moat stocks from 2002 to 2014 using the Morningstar Direct stock database. All the wide moat stocks are used to create a portfolio starting in June 2002 and then updated every year based on the new list released by Morningstar. Both equal and market cap weighted indexes are formed for the portfolio backtest. The results were striking.