Ideastorm #7

The golden age of investing, loss aversion theory, index inclusion, and more...

Welcome to the latest Ideastorm. Market Sentiment curates the best ideas and distills them into actionable insights. Join 37,000+ others who receive curated financial research.

Actionable Insights

If you believe in mean reversion, the golden age of investing is almost certainly over, and you will not enjoy anything like the returns your parents made.

Based on the loss aversion theory, an investor who closely follows the markets will be deeply unhappy even if they make great long-term returns.

S&P Global analyzed all additions and deletions to the S&P 500 from 1995 to 2021 and found the index effect to be in structural decline.

There is a significant and positive relationship between stock age and stock performance.

1. You might not make the returns your parents made

Even after accounting for Black Monday, Dot-com bubble, Global Financial Crisis, and the COVID-19 pandemic, global equity investors enjoyed an annualized return of 7.4% from 1981 to 2021. This was 72% higher than the annualized return of 4.3% from 1900 to 1980.

The global bond market also provided an incredible tailwind for the portfolio of someone who started investing in the ‘80s.

Annualized return of Global bonds from 1981 to 2021 — 6.3%

Annualized return of Global bonds from 1900 to 1980 — 0% (yes, that’s not a typo!)

If you believe in mean reversion, the golden age of investing is almost certainly over, and you will not enjoy anything like the returns your parents made.

But rather than trying to perma-bear like Michael Burry, understanding this can help us plan better for long term investing.

Including both the lacklustre years before the 1980s and the bumper ones thereafter, these long-run averages are 5% and 1.7% a year for stocks and bonds respectively.

After 40 years of such returns, the real value of $1 invested in stocks would be $7.04, and in bonds $1.96. For those investing across the 40 years to 2021, the equivalent figures were $17.38 and $11.52. — The Economist

If you are young and choosing a long-term investment goal, it’s better to be conservative and go with the long-run average return instead of focusing on the returns of the past few decades. i.e., assume a 5% CAGR for the stock return instead of the 7.5% we have seen over the past 40 years.

If you are right, you will hit your goal. If you are wrong and the next few decades also generate outsized returns, you will be pleasantly surprised by a bigger portfolio at the end.

Source:

How the young should invest — The Economist

Investing Amid Low Expected Returns — Antti Ilamanen

2. The problem with obsessing over stock prices

The S&P 500 has returned nearly 300% in the last 25 years — But the market closed in green only on 53% of the trading days. This small edge, compounded over a few decades, is what matters in investing.

If you follow the markets daily, you will encounter the behavioral economics phenomenon of loss aversion. It’s where a loss is emotionally more severe than an equivalent gain. For instance, the pain of losing $100 is far greater than the joy gained in finding the same amount.

Based on the loss aversion theory, if we assign a +1 happiness score if the markets end in green and a -2 if the markets end in red, we see that someone who checks the market daily will be deeply unhappy no matter the gains.

In his book Fooled by Randomness, Nassim Taleb highlights that a 15% return with 10% volatility translates to a 93% probability of success in a given year. But, the probability of success drops to 54% if we evaluate the investment daily. In other words, give time time!

I never spend any time thinking about the daily stock price.

At almost every all-hands meeting I say: 'Look, when the stock is up 30 percent in a month, don't feel 30 percent smarter. Because when the stock is down 30 percent in a month, it's not going to feel so good to feel 30 percent dumber.'

- Jeff Bezos

3. Index Inclusion Effect

Uber is set to join the S&P 500 index on December 18.

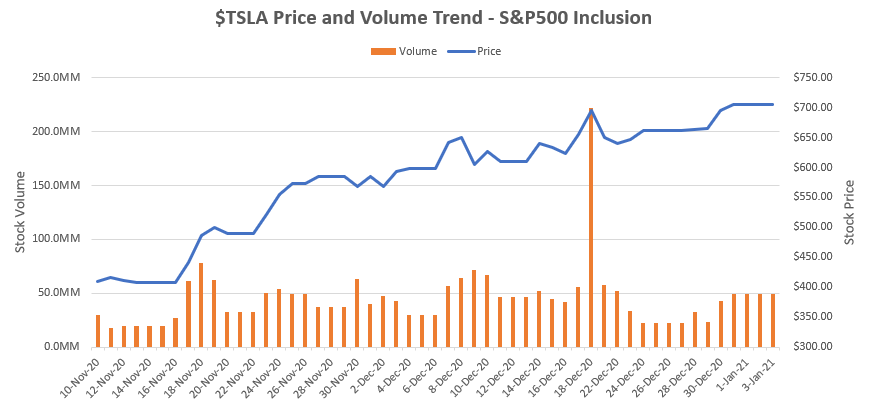

Given the exponential growth of passive indexing over the past few decades, investment inflow to the S&P 500 is now at its highest in history. In theory, when a new stock is added to an index, all the funds that track that index must buy that stock, creating buying pressure (and vice-versa for stocks removed from the index).

A classic example to support this effect was Tesla’s addition to the S&P 500. Tesla was the largest company to be added to the S&P 500 at a valuation of more than $500 Billion. The inclusion of Tesla into the S&P500 was announced on 16th Nov 2020, and the date of inclusion was 21st Dec 2020. There was a 6% jump in stock price and almost 4x normal traded volume on the day of index addition.

While this might look tempting, recent research indicates that the index inclusion effect is becoming weak.