Ideastorm #16

Keyman risk, is Buffett's alpha skill or luck, the illiquidity premium, and more...

Data is great, but data distilled into charts can drive home an insight even better. One newsletter we really love is our friend Callum's Weekly S&P500 Chartstorm which curates handpicked charts with clear commentary, saving you time and helping uncover hidden insights.

This week's Chartstorm is a special issue that puts together timeless charts with a focus on the biggest risks and opportunities in the coming years. You can check out the special pack here and subscribe:

Actionable insights

Stock prices of companies have consistently shown short-term fluctuations during unexpected deaths of CEOs and executives. This is increasing with time.

Most of Warren Buffett’s consistent outperformance of the market can be systematically explained by a disciplined application of investment factors.

Emerging markets have more “alpha” due to unexploited inefficiencies – despite higher transaction costs.

Illiquidity is also a form of risk, and carries its own premium. Higher returns of value investing portfolios might be a result of their illiquidity, and it’s crucial to separate the illiquidity premium from the perceived value premium.

Keyman risk

While most people claim that they're long-term value investors, they are truly tested when unexpected events occur. Here's how the market reacted to some news events:

When Elon Musk appeared on Joe Rogan's podcast and took a puff of marijuana, two of his key executives resigned, and Tesla's stock crashed by 9% in a single day.

Papa Johns's founder John Schnatter resigned in 2018 following a controversy related to using a racial slur. The stock dropped by more than 13% from its all-time highs before bottoming out.

Apple shares fell by more than 5% following the death of Steve Jobs.

The reputation of many companies seems to be tied to the actions and fortunes of "star CEOs". An average of 7 CEOs of publicly traded companies die every year, and it’s a serious question whether this has any long-term effect.

Research by Quigley and Hambrick of the University of Georgia revealed that since the 1950s, the perception of company performance has been increasingly affected by the perception of the CEO. Quigley and two other associates went on to study how unexpected CEO deaths affected shareholder perception of the company, by looking at stock market performance. In a study collating over 2,000 executive deaths between 1950 and 2009, they zeroed in on 240 deaths that were "unexpected" and studied how they moved the market. They found:

The market didn’t show any significant positive or negative bias towards the unexpected death of CEOs. The mean "Cumulative Abnormal Return" (CAR) was slightly negative (~ -0.5%) and did not change much with time.

However the absolute value of the CAR following 1 to 3 days after the death has increased over the years, showing that markets are more sensitive to these events. 1 day CAR has increased from 2.35% in 1950 to 6.41% in 2009. 3 day CAR has increased from 3.02% to 7.89% in the same period.

In general, there has been a consistent increase of 0.08% in the absolute value of the CAR every year. Standard deviation has also increased.

They noted a definite increase in volatility around unexpected CEO deaths. Over the course of 60 years, the shift in market value caused by an unexpected CEO death increased by approximately $65 million (in 2009 U.S. dollars)!

Buffett's Alpha: Skill or luck?

Warren Buffett is now more myth than man... I think that we do a disservice to Buffett, when we put him on a pedestal and treat every word he says as gospel.

– Aswath Damodaran, Dean of Valuation

Warren Buffett has developed a reputation for having a Midas Touch among investors. Having compounded Berkshire’s stock at 19.2% per year to deliver a whopping 4,384,748% return over the last 59 years, Buffett has developed something of a cult around himself. Yet, some critics and skeptics suspect that while Buffett was definitely an above-average investor, he also benefited from an era of free cash and dollar supremacy.1

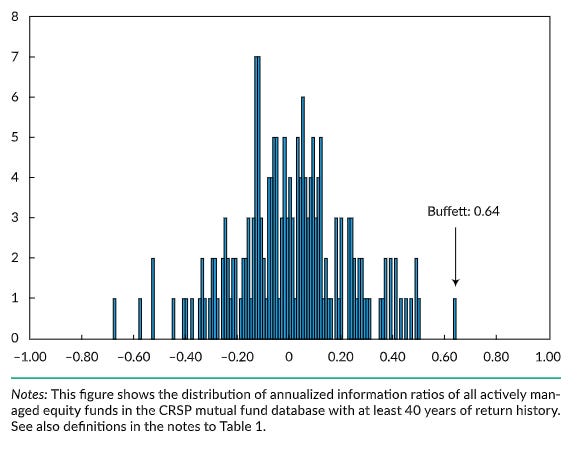

In 2012, three investors from AQR Capital published a paper named "Buffett's Alpha" that systematically deconstructed Buffett's method to see if it could be replicated. The first surprising thing was that Buffett’s portfolio had a Sharpe Ratio of 0.64 – far ahead of most mutual funds in the 40 years prior with high average returns, but nothing supernatural, experiencing periods of underperformance and drawdowns as well.

Then what explained his excellent track record? The researchers discovered that a majority of Buffett's returns could be attributable to a disciplined investing approach that relied on a few factors: