How much risk can you handle?

You can’t manage what you can’t measure.

We have no paywall on this report.

Here is a fun quiz:

And no, a 100% stock portfolio is definitely not “moderate.” When asked this question, most of us would answer based on intuition. Even financial advisors use simple heuristics, like older means safer investments and younger means more equities, without capturing your unique risk profile.

So, we created a free short quiz1 based on this landmark study. It helps you accurately identify your risk profile for investments. Almost everyone we shared this quiz with was surprised by their score!

The 2008 financial crisis took almost everyone by surprise — even those who were supposed to guide others. In 2011, the Wall Street Journal published a harrowing story of how Carl Richards, a financial advisor, lost his home in the aftermath of the GFC.

Carl's mistake was simple. Like everyone else at the time, he expected the housing market to continue rising and stretched himself too thin by buying an expensive house.

We borrowed 100 percent of the purchase price. In fact, I was told I could borrow even more if I wanted. I had perfect credit and a solid income that was growing.

I should have known better. No matter how well things are going, borrowing 100 percent of the purchase price of a home is not a good idea. I shouldn’t have relied on someone else to make that calculation, let alone the guy who was making money putting me in the loan. I was a financial adviser, and I never sat down to figure out what it would take to make this work.2

Finally, when the crisis hit, Carl’s income went down 20 percent (advisor business is based on AUM), and at the worst possible time, health insurance, property taxes, and mortgage all went up. Unable to afford the interest payments, they finally had to put up their house in a short sale.

I’ve also learned some things about risk. Risk is an arbitrary concept, until you experience it. And I’ve noticed myself focusing more on the consequences of something going wrong than just the probability of that happening.

Most of us think that we can handle the risk we take with our portfolios, but data shows a different story. Following the 2008 financial crisis, 57% of U.S. households investors reduced their equity holdings. This decision to lower equity holdings after a steep market decline made sure that they solidified their market losses and missed out on the subsequent recovery3.

The story is not very different during good times, either. Barring the brief Covid crash, the market has not faced any significant correction in the last 10 years. Still, according to Morningstar Research4, investors lagged the overall market by 1.1% every year. This gap in return was due to investors selling when the market was low and buying back in once it had recovered.

What’s your risk profile?

Ultimately, panic selling and trying to time the market during crises result from taking more risks than you are comfortable with. Take a look at how the S&P 500 performed from 2000 to 2010 and from 2010 onwards. After the 2008 crisis, markets have mostly gone up, creating a false sense of security and pushing investors into riskier portfolios.

But, having a risky portfolio only offers a prospect of higher return — Not a guarantee.

The traditional way of classifying the risk of an investment is by just measuring its volatility. If the asset prices swing wildly, we consider the investment too risky. But when you think about it, no one ever makes an investment decision just based on volatility. You would rarely hear someone say — “I won’t invest in that stock because the prices fluctuate so much.”

What everyone is really worried about is the chance of capital loss.

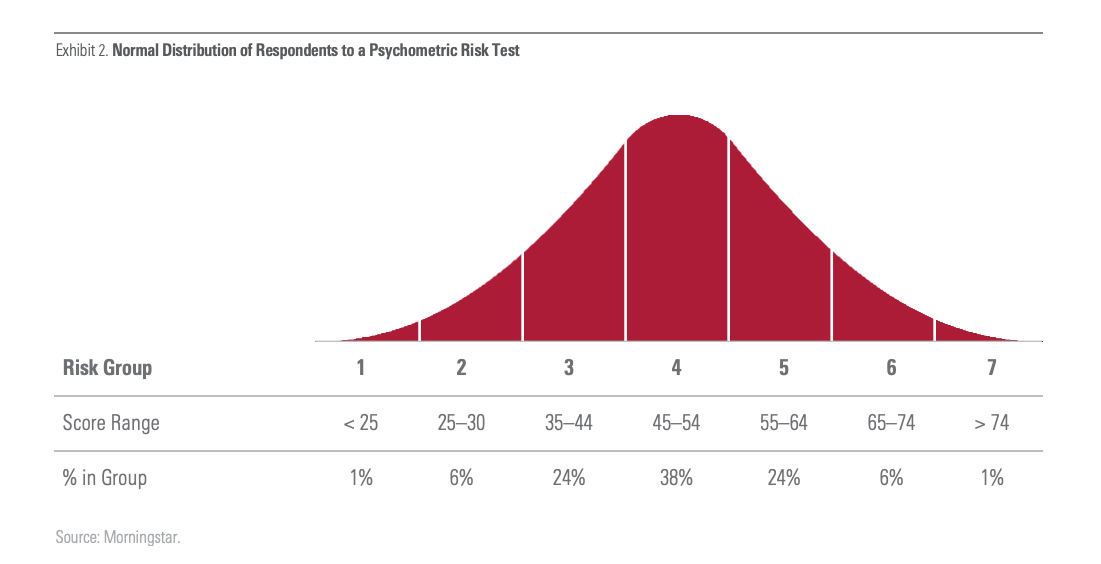

And if you believe that a significant capital loss wouldn’t affect you, you’re probably fooling yourself. Based on Morningstar’s risk profiler that was taken by millions of respondents over the last two decades, investor’s risk profile follows a normal distribution, and <10% of investors can be classified as truly aggressive investors.

The good news is that once you determine your risk profile, it will remain largely the same. When tested, investors who experienced the Global Financial Crisis scored very close to what they scored before the crisis5.

How much risk should you take?

The amount of risk you should take is directly proportional to your risk profile and the rate of return required to achieve your investment goals.

If you are a conservative investor looking for 4% long-term returns, consider safer investment options like bonds, real estate, or the permanent portfolio.

If you are an aggressive investor who is expecting 7%, it’s better to tilt your portfolio towards riskier assets like stocks, leveraged ETFs, and private equity.

For what it's worth, it's better to err on the side of caution. Even if you are an aggressive investor, if you only require a 4% return to achieve your investment goals, it is better to have a conservative portfolio. That’s why even the top 1% of investors, with a median of $1M in their portfolio, invest only ~60% in stocks. Finally, no matter how aggressive your risk profile is, if your expectation is a 15 or 20% CAGR, it's better to revise your expectation to more reasonable returns rather than to take more and more risk with your portfolio.

It’s also important to understand whether you are taking compensated or uncompensated risks. Equities, on average, are more volatile than bonds. But at the same time, they provide a higher return over the long run. In this case, the extra risk you are taking by investing in equities is compensated by the higher expected returns of equities.

However, the same cannot be said if you invest in individual stocks. While individual equities are easily an order of magnitude riskier than fixed income, they rarely provide the return to compensate for this extra risk.

One of the most critical factors to consider before finalizing your portfolio is downside risk.6 If you are confused between, say, a stock-only portfolio vs. a 60/40 portfolio, more than just focusing on the returns, consider the portfolio drawdowns.

Compared to the S&P 500, the 60/40 portfolio experienced only half the drawdown during periods of market stress. In addition, it recovered ~40% faster than an all-equity portfolio.

Even if you have a high-risk profile and are comfortable with a 50% drawdown, it’s worth looking into how you traded during the last market drawdown to see whether you stuck to your plan.

After all, there's a difference between knowing the path and walking the path.

If you made it this far, chances are you gained at least a few insights that will help you make a smarter investor. If you would like to receive reports like this frequently and get access to our full research, consider becoming a paid subscriber! Thank you :)

We also offer lifetime memberships, which give you access to our universal repository. This ever-evolving document contains our ideas, high-quality corporate and academic research, data sources, datasets, newsletters, and blogs we read for inspiration, research, and various financial tools.

Footnotes

Fun fact — The website was designed by AI (bolt.new) | I just gave the requirements, and with some fine-tuning, I had the website up and running in a few hours.

[emphasis by author, edited for brevity]

These questionnaires that use $$ rather than percent of capital make no sense to me. At $1000 I will be looking purely at present values of returns, but ask me about 50% of my capital and emotions and risk appetite start to matter. Also, 100% equities in Berkshire Hathaway is different that 100% in small cap or tech stocks. Both these options are classified as aggressive. I don't agree that they should be the same.

"While individual equities are easily an order of magnitude riskier than fixed income, they rarely provide the return to compensate for this extra risk."

💯 https://blog.inverteum.com/p/individual-stocks-fools-game