Buffett's Alpha: Skill or Luck?

What you can and can't mimic

Hello there! Quick announcement:

For the first time in two years, we are taking some time off. Market Sentiment will be on a break for one month, starting today. We are pausing billing for this month. Monthly subscribers will NOT be charged for this month, and this month WILL NOT count toward billing for annual subscribers.

We have some exciting articles in the pipeline, and we’ll see you in July! Happy 4th of July in advance :)

The Efficient Market Hypothesis roughly says that the prices of assets in the market reflect all available information, and picking stocks is a loser’s game. It isn’t taken seriously by most in the investing world right now, but when the theory gained traction in the mid-1960s, academics used it to ridicule active management citing years of abysmal performance. Yet there were exceptions to the theory that were hard to reconcile: Chief among them was Warren Buffett.

Buffett’s track record was a problematic counter-example, and most academics dismissed it as a freak incident1. William Sharpe called it a “3-sigma event” that was a statistical outlier. Things came to a head in 1984, when Columbia Business School brought Warren Buffett and Professor Michael Jensen face-to-face. Jensen argued that if a bunch of analysts do nothing but flip coins, some would eventually toss ten heads in a row, but that did not prove that the analysts had talent in flipping coins. Buffett used the same premise to argue that in a National Coin Flipping contest, there would definitely be people who turned up ten heads in a row and even “orangutans” might produce the same result – but if all the orangutans came from the same zoo, surely there was more to it than luck?

Buffett then shared the results of nine money managers who came from the “intellectual village of Graham-and-Doddsville” who had different styles of investing and little overlap among their portfolios, but had spectacular long-term records.2 Wasn’t there a method to their madness if they shared common principles?

Since then, the question has remained: Is Buffett’s method replicable? While he humbly states that anyone could do what he does, would his principles hold today? Was he just born in the right place at the right time? How are his operations structured to give him unique advantages?

Today’s report dives deep into academic research and studies that break down Buffett’s superior performance into four pillars:

Investing framework

High-level structure

Skills

Luck

While the investing framework would have actionable insights for every investor, it’s important to know the high-level structure that gives him advantages over retail investors. And let’s be real – there’s no way you can replicate Buffett’s unique skills and the personal luck that gave him an edge. It’s important to know what these are so that you don’t aspire for factors you have no control over.

Investing framework

A 2005 paper named “Imitation is the sincerest form of flattery” studied Buffett’s outperformance in a unique way:

It noted that the majority of Berkshire Hathaway’s returns were attributed to a concentrated portfolio of large-cap stocks, with 73% of the company’s holdings being held in 5 stocks.

It backtested the performance of a hypothetical portfolio that mimicked the investments of Berkshire the following month, and discovered that it still generated 10.75% abnormal returns over the period 1976 to 2006!

This study suggested that Buffett’s outperformance wasn’t a result of luck or timing, but it didn’t reveal anything further about market factors, leverage, performance of public and private portfolios, etc. To understand this further, Frazzini, Kabiller, and Pedersen of AQR Capital decomposed Berkshire’s portfolio from 1976 to 2017 and published their results in a paper named “Buffett’s Alpha.”

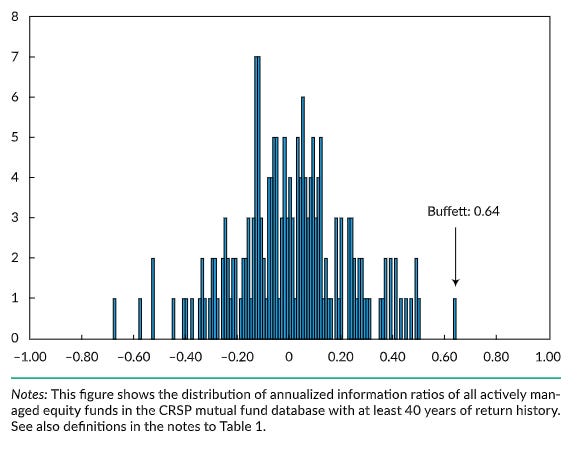

First, they benchmarked Buffett’s track record against other mutual funds and public stocks – and it placed in the top 3% and 7% respectively. But by restricting the universe of funds/companies to those that had survived for 40 years or more, Buffett’s performance had the highest Sharpe ratio and Information ratio of any asset.

Then the team analyzed Berkshire’s portfolio in terms of “factors”: market risk, small vs large cap premium (SML), value vs growth premium based on book value (HML), momentum (UMD), and quality (QMJ). In addition, the researchers included “betting against beta” (BAB), a factor that indicated how much of the portfolio was invested in high-risk stocks. Buffett’s portfolio showed the following characteristics:

Beta of less than 1 compared to the market (less risky).

Through all periods, the SML factor was negative, indicating a preference for large-cap stocks.

No significant UMD – Buffett neither followed trends or went against them.

High HML, showing that stocks with high book value relative to market value were preferred.

Though interesting, the alpha across these periods was not explained by the four factors above – i.e controlling for these factors did not significantly affect the portfolio performance. But the two other factors made a difference:

High correlation with QMJ (High-quality stocks)3

High correlation with BAB (Safe stocks)